Marketing & Sales

In Housing's New Normal Rules, Supply And Demand Matter Less

For what comes next in market-rate housing -- given low supply and what will become pent-up demand -- count on experts to talk of slowdowns, softness, downturns, etc. in terms of letters: V, L, U, W, and K. After that, a boom resumes.

If the cure for high prices is high prices, it stands to reason that a cure for 20% year-on-year price increases in existing home transactions might be strong medicine. You might say cathartic.

The low inventory-high demand dynamic in housing has come to this:

U.S. home prices continued to advance at a very rapid pace in February,” says Craig J. Lazzara, Managing Director at S&P DJI. “The National Composite Index recorded a gain of 19.8% for the 12 months ended February 2022; the 10- and 20-City Composites rose 18.6% and 20.2%, respectively. All three composites reflect an acceleration of price growth relative to January’s level.

...

“The macroeconomic environment is evolving rapidly and may not support extraordinary home price growth for much longer. The post-COVID resumption of general economic activity has stoked inflation, and the Federal Reserve has begun to increase interest rates in response. We may soon begin to see the impact of increasing mortgage rates on home prices.”

Until now, focus has been on the causes of the squeeze in supply that have, in turn, caused prices to skyrocket.

Now, focus will isolate on whether prices that have defied and disconnected from gravity will in fact be unsustainable, and cause their own array of consequences. Or perhaps whether, after chiseling away at a clamoring wave of demand, they [inflation and interest rate fueled high prices] will do one of two things: 1) hold up as a metering tool to cadence demand for a continuously heavily governed supply of new homes, or 2) cause a disinflationary reversal in demand, leaving built but unsold inventory standing.

If high prices cure high prices, logic says the cure should cause unsustainably high home prices to fall.

Trouble is it's all well to conclude that "something's got to give."

The outcome most imagine – as what exactly has got to give – is a fall-off in demand. Will that fall-off in the numbers of intensely-motivated buyers cause prices to retrace downward? That's doubtful for three reasons.

- demographics

- rents

- cost of sales

Let's take a look at each of those reasons.

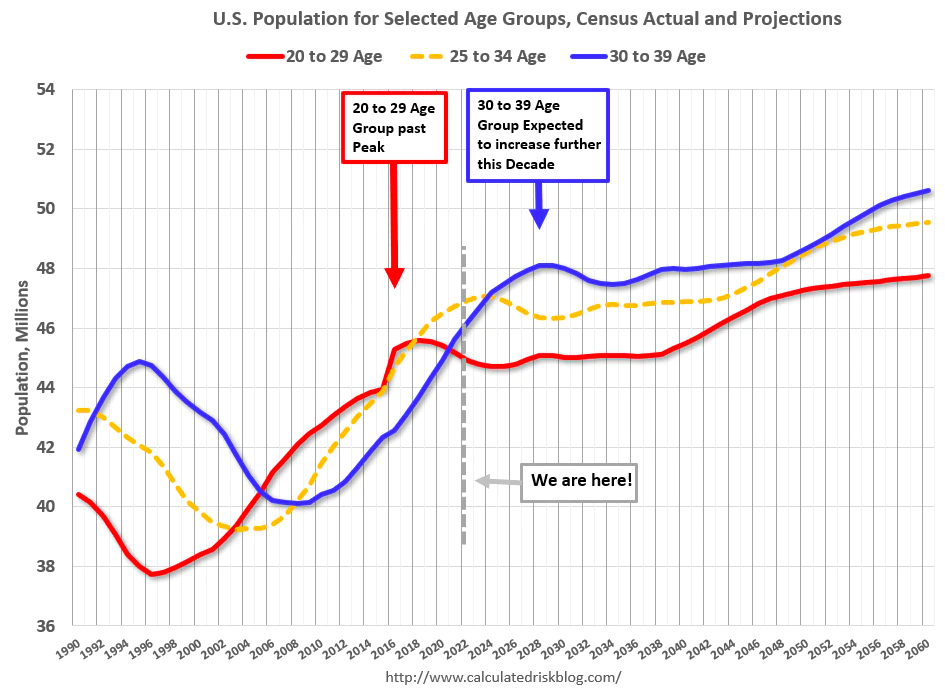

Key insights on Housing and Demographics, from Calculated Risk's Bill McBride are here, and they contain sharp, albeit nuanced, insights for residential new construction stakeholders.

For home buying, the 30 to 39 age group (blue) is important (note: see Demographics and Behavior for some reasons for changing behavior). The population in this age group is increasing and will increase further over this decade.

The current demographics are now very favorable for home buying - and will remain somewhat positive for most of the decade, although most of the increase is now behind us.

McBride's distanced, long-haul view is that demographics and housing markets harmonize in correlation to one another across greater spans of time. His caveat focuses on household formation rates as a wild card that can throw off the strong correlation and "overwhelm demographics in the short term."

Like now, maybe. Market-rate home sales rode a young-adult Baby Boom wave until the 1979 to 1983 period, when a Paul Volcker-led Fed jacked up interest rates to fight inflation.

Now, what about rents? If prospective homebuyers want to seize leverage in their bid to use their might to bring down the prices of homes, they're going to need convincing alternatives to ownership to convince sellers they can walk away from buying a home and still be happy with their home choice.

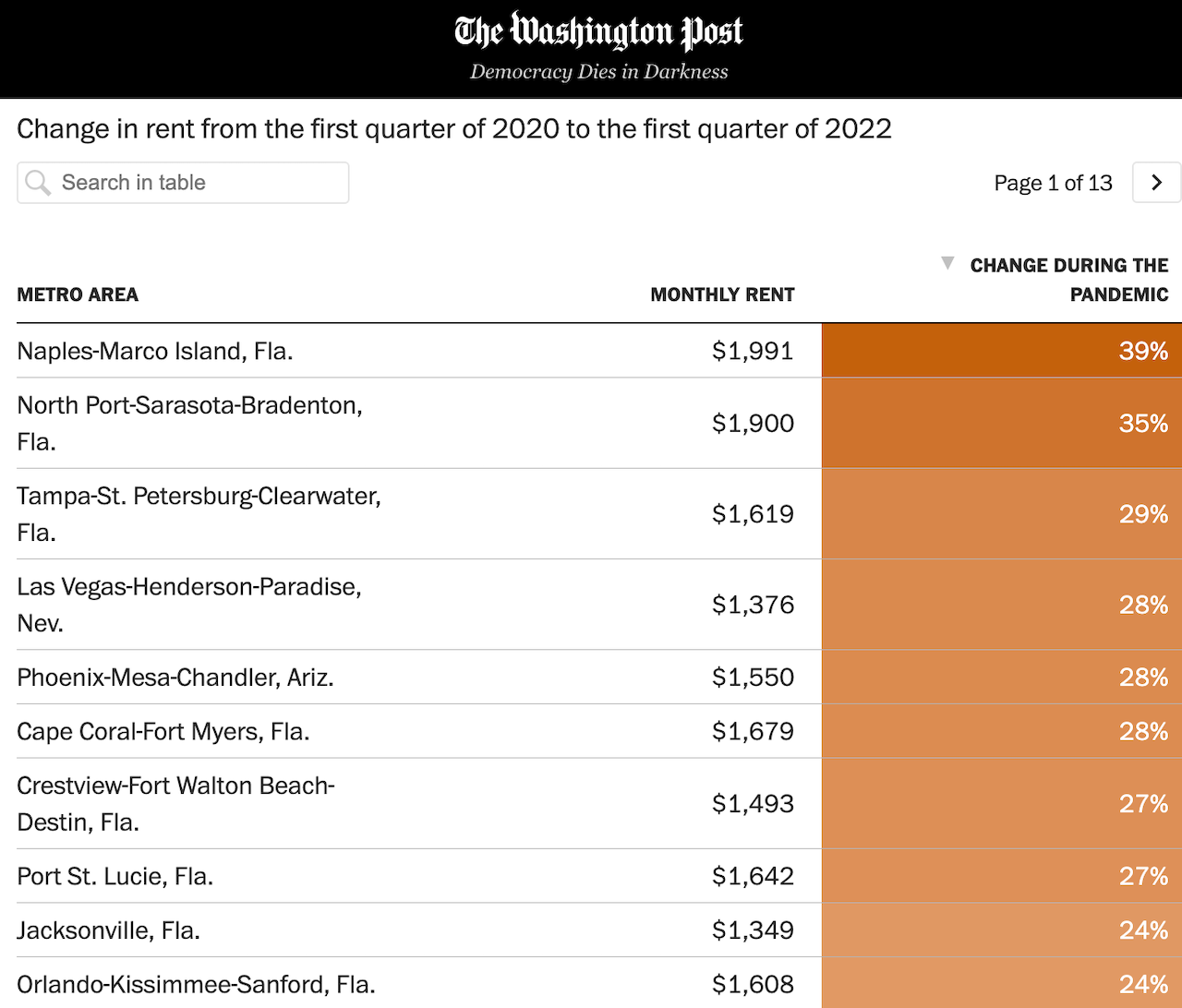

That's difficult in this environment, as this recent piece in The Washington Post illustrates:

Nationally, rents rose a record 11.3 percent last year, according to real estate research firm CoStar Group. That fast pace of growth remained elevated in the first months of 2022, as many parts of the country continued to notch double-digit jumps in rent prices.

“A supply-demand mismatch is making rents unaffordable,” said Dennis Shea, executive director of the J. Ronald Terwilliger Center for Housing Policy at the Bipartisan Policy Center. “The lowest-income families are being hardest hit by rising rents and a lack of supply.”

Single-family rental – the so-called more attainable alternative to homeownership – offers no panacea either for consumer households looking for leverage with prospective homesellers, new and resale.

- Nationwide, single-family rent prices were up 13.1% year over year in February, the 11th straight month of record-level gains

- The gap in growth between the lowest- and highest-priced rental tiers closed in February, with respective annual gains of 12.7% and 12.8%

Plus, now that inflationary pressures are forcing landlord and property management costs higher, rent vs. own as a choice is going to compare even less favorably. So, where does that leave us in the "cure-for-high-prices-is-high-prices" continuum, given that more consumer households would be looking to own based on demographics, and fueled by inflationary erosion of their own pocketbooks as rent increases kick in?

It leaves us at the crux of the supply-constrained matter and it's this: while home construction may be ripe for cost and price disruption, no single disrupter currently offers a way around the reality that homebuilder's cost of sales and razor-thin margins mean just one thing.

If they – the homebuilders – are going to operate price-cost neutral, they're going to have to keep ratcheting up prices even as they see their pace of absorptions and waiting lists, and traffic counts start to show wear and tear, and their incentives start to multiply as interest rates siphon off buyers who can't keep pace with qualifications and monthly payments.

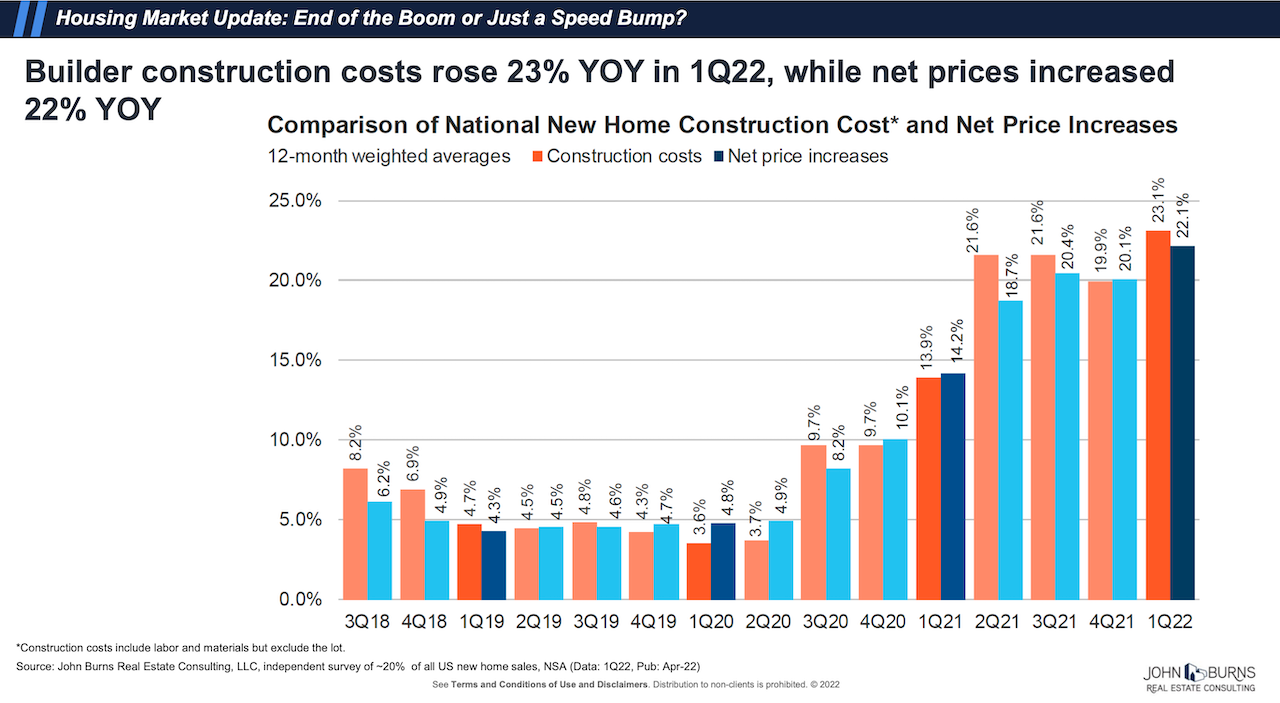

Going back to that high prices shocker earlier, there's only one set of figures more staggering and astonishing than 20% year on year price increases – actually median prices for new homes were up 21.4% y-o-y, March of 2021 vs. March '22 – and that's this: Builder's construction costs. Here's how that looks across a pre-pandemic through the present time frame, according to John Burns Real Estate Consulting:

What's more, this data tends to skew toward larger, high-volume production builders with greater clout among vendor suppliers, and with more ways to pull through their costs with volume.

For the lion's share of homebuilders – small companies, a prospect of cost-price neutrality is even more challenging.

A new National Association of Home Builders Builders’ Cost of Doing Business Study notes that among its sample homebuilder firms, there's very little margin to work with on the cost side, ruling out flexibility on pricing.

Builders’ profit margins declined in 2020 for the first time since 2008. As Figure 2 shows, their average gross margin fell dramatically during the housing recession (from 20.8% in 2006 to 14.4.% in 2008), but then rose steadily through 2017 (19.0%) before edging lower in 2020 (18.2%). Similarly, builders’ average net margin plummeted between 2006 and 2008 (7.7% to -3.0%), gradually increased through 2017 (7.6%), and then slipped back in 2020 (7.0%).

Long and short of it, it's tough to imagine how this time rules of supply and demand can play out in such a way that the cure for high prices will be high prices.

Wild cards might be one we've noted and one, given the parallel universes of down and dirty and messy world homebuilding and real estate next to the apparently gravity-free metaverse of Silicon Valley corporatocracy, we should mention.

- As Calculated Risk's Bill McBride cautions, we may have entered a "short-term" window where forces can "overwhelm demographics" and, somehow, rein in household formation (more multigen, adult kids in basements, double- and triple-ups, etc).

- Elon Musk could buy a top 5 ranked homebuilder and develop an automated, roboticized, industrialized, modern manufacturing infrastructure to produce carbon-neutral, high-design, homes and communities on land he could also by taking over a Starwood or a Brookfield.

He appears to have time on his hands for such imaginings.

Join the conversation

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Marketing & Sales

Why Homebuilders Should Stop Ignoring the Move-In Moment

Buyers don’t just want a new home — they want a seamless handoff into it. Concierge services may be the zero-cost amenity that becomes a new industry standard.

When Homebuyers Pull Back, Builder Brands Must Step Up

In markets under stress, consistency, empathy, and value-driven messaging provide builders with a critical edge among today’s cautious buyers. Advisor Barbara Wray gets real about the path forward for homebuilders today.

What Separates Homebuilders Thriving Amidst 2025’s Chaos

Builders face rising stakes to unify tech, data, and operations or risk falling behind amid affordability, insurance, and labor challenges.