Policy

Tighter Policy Makes For A Rough Go Near-Term — But It's Needed

A recipe to stave off disaster two years ago could become one if policymakers don't create conditions for the 'invisible hand of the markets' to restore balance.

New York City real estate investor and developer Seymour Durst studied accounting at the University of Southern California before in 1940 he joined the firm his immigrant father Joseph founded in 1915, with money he set aside from work in New York's garment business. With a belief that no one should buy anything one could not walk to, Seymour worked his way up at the Durst Organization, taking control of the company after his father died in December 1973, and building a New York City centric empire.

Seymour Durst, who died in 1995, left a legacy – famed and infamous – that spans well beyond New York real estate. One of those legacies is the National Debt Clock, which Seymour invented, and minded like it was a grandfather clock in the den up until the week before his death in 1995.

If it bothers people," Seymour Durst was said to have uttered, "then it is working."

Mechanically, the National Debt Clock -- like its digital offspring, U.S. Debt Clock.org – connects the dots of its running display most emphatically from the gross national U.S. debt to each American citizen and taxpayer's share of that debt.

Said Seymour Durst:

We're a family business. We think generationally, and we don't want to see the next generation crippled by this burden."

Fast forward to now. The clock Durst set in motion spools up in the $30 trillions, and with it M3 money supply, which measures the economy's money supply in its broadest – stored valued – terms.

Since 2000, M3 money supply has expanded 368%," Tony Avila, ceo and Managing Principal of Builder Advisor Group and Encore Capital Management told homebuilding and real estate investment executives at BAG's annual housing forum last week. "[M3 supply expanded] 42% since January 2020. Such rapid expansion in the money supply is caused by loose monetary and fiscal policy which is an indicator of more inflation in the future and higher rates."

In the context of 24-plus months where COVID-19 made the rules mortals either obeyed or defied them, all the money that was viewed as needed to stave off calamity and collapse is now looked at as the opposite. In other words, all that easy money could now cause a nasty turn of financial and economic events if the Federal Reserve and government don't pull off the policy-equivalent of the 2009 landing of US Airways Flight 1549 on the Hudson River.

The late-Spring 2022 business and economic backdrop contrasts so sharply with the prior 24 months that a wholesale fiscal and monetary policy U-turn from pandemic era rescue to inflation and interest rate fire-drill, some evidence of which we may see in the release today of the minutes of the recent Fed meeting.

Here's a take on today's FOMC Minutes, from Bloomberg. [gift link]

Homebuilders and their partners remain hyper-focused on still-clamoring demand for every new home builders can bring across the the construction cycle finish line, and a wealth of evidence supply can not meet nearly a normal level of demand, and structural demographics underlying all that demand.

For many of them – given the absence in today's operating environment of shadow land inventory and strong governors on land entitlement, permitting, and development – inflation, interest rate surges, and sweeping geopolitical risks simply don't amount to signals of a crash.

That doesn't mean that another 10% increase in new home ASPs, a fast-approaching 6% 30-yr fixed mortgage interest rate, and the collateral effects of corrosive inflation on consumer behaviors and attitudes couldn't scorch any number of homebuilder operators with the burn of having the wrong products in the wrong locations at the wrong prices for a much, much diminished stream of demand.

So, maybe not a crash, but a long, slow burn that could stifle demand and choke economic growth.

For precedents that might be instructive, Avila's economic research team at BAG looked historically at periods of skyrocketing inflation – including the mid-1970s energy crisis and the period during which then-Fed Chair Paul Volcker battled high-teens inflation and stagnant economic growth.

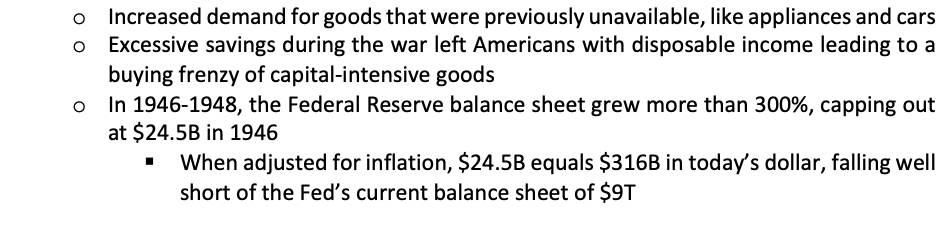

The post-World War 11 years, between 1946 and 1949, lend themselves to a fair comparison, Avila notes, as a rush of demand collided with hard constraints on supply chains. Among Avila's key observations are that household demographics and family and job formations after the war resembled, in ways, current fundamentals for a strong economic period ahead:

During that period, Avila notes, "the invisible hand of the market" – unaided by policy accommodation – kicked into high gear, tamed inflation, and ignited productivity and massively-retooled capacity able to keep pace with consumer spending and demand.

The hard choice – and one that Seymour Durst had in mind when he spoke of not wanting to see "the next generation crippled by this burden" – is for both policy makers and private sector leaders to get the economy's "house in order."

The outlook for this year, and near term demand is still very good," says Avila. "When we peer around the corner at 2023 and beyond, we've got to make choices that will secure the health of the markets for that next generation."

Join the conversation

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Policy

Can Ditching the Car Unlock Pent-Up Housing Demand?

A car-free lifestyle could help homebuyers afford more — and give developers a powerful new lever near transit hubs. It's part of a 'missing middle' solutions set.

California Breaks CEQA Barrier To Reignite Housing Production

Championed aggressively by Gov. Gavin Newsom, the historic environmental law reform unlocks the potential for infill housing—and could become a model for other high-barrier states.

Governor’s Veto Derails Connecticut Upzoning Push

State leaders aim to regroup for a fall special session after a housing bill faces resistance from local zoning defenders.