Policy

In Market Talktrack, Uncertainty, Even Concessions Crop Up

Two terms have surfaced in the spotty, choppy limbo market dynamic that has checked up both construction flow and demand mojo: Pause and Concessions.

A summer of uncertainty has settled across active homebuilding markets in the U.S., like a naggingly warm blanket.

The feeling something beginning to shift in the business environment brings to mind an unforgettable line Ernest Hemingway coined in "The Sun Also Rises" to help the uninitiated get how a character of his went broke.

How did you go bankrupt? Two ways: Gradually, then suddenly.

Two terms crop up in the context of new home sales activity we haven't heard since well before the pandemic struck last late-Winter, and set in motion a surreal, gravity-free trajectory of hyper demand for every new structure that could be built.

- Pause is one of them.

- Concessions is the other.

Pause, many believe and want to believe, is a natural inevitable side-effect of the suspended animation of supply chain disruption, schedule bottlenecks, and delivery-date challenges that have laid siege to work-streams nearly everywhere. Pause describes a status somewhere between intent and reaction, where questions of who's causing it and who's affected may not matter as much as the fact that the pause simply exists – and one hopes it is precisely that – a pause.

Concessions, on the other hand, reflect measures that are taken when the strategic conviction may be that a pause now says something more structural about the market.

In some markets, we hear, concessions have entered the sales "toolbox" as a way builder sales associates now work to rekindle more predictable inventory absorption rates a) because prices may have skidded past their points of elasticity in the past couple of months, and b) because buyer prospect fatigue and frustration levels have begun to dampen some of the urgency and motivation some of those buyers had earlier.

Clearly, an inflection in momentum has arrived.

Hemingway might describe the tipping point as he inimitably characterized going broke: Gradually, then suddenly.

Now, here's a couple of offset considerations that struck at our sense of curiosity, and we thought, may shed helpful light on this context of a "pause" and of a need for "concessions."

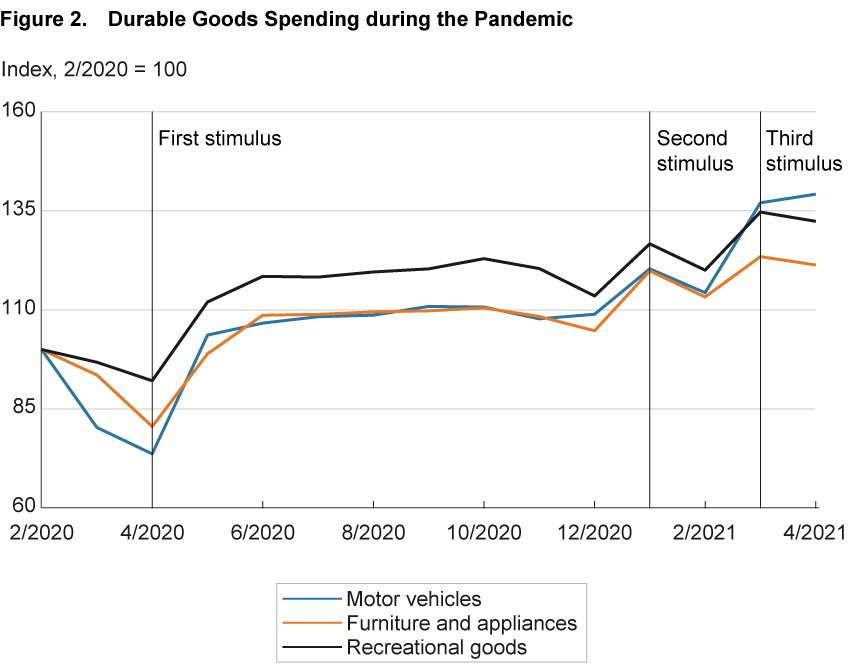

One is a simple plot-line of durable goods demand in the time of the pandemic – here from Cleveland Federal Reserve research analyst Kristen Tauber and senior research economist Willem Van Zandweghe.

The pandemic may have lifted the demand for durable goods directly, by shifting consumer preferences away from services toward a variety of durable goods. It may also have stimulated spending on durable goods indirectly, by prompting a strong fiscal policy response that raised disposable income. We estimate the historical relationship between durable goods spending and income and find that income gains in 2020 accounted for about half of the increase in durable goods spending, indicating that the direct and indirect effects of the pandemic on durable goods spending were about equally important.

If as much as half of consumer zeal and mojo for spending on durable goods owes to not one, not two, but three separate stimulus programs that bolstered disposable income at the same time that interest rates have been historically low, then, possibly, the stimulus effect may now have begun to run its course on demand momentum.

Not all at once, mind you, but gradually, in spotty markets, and in a choppy way.

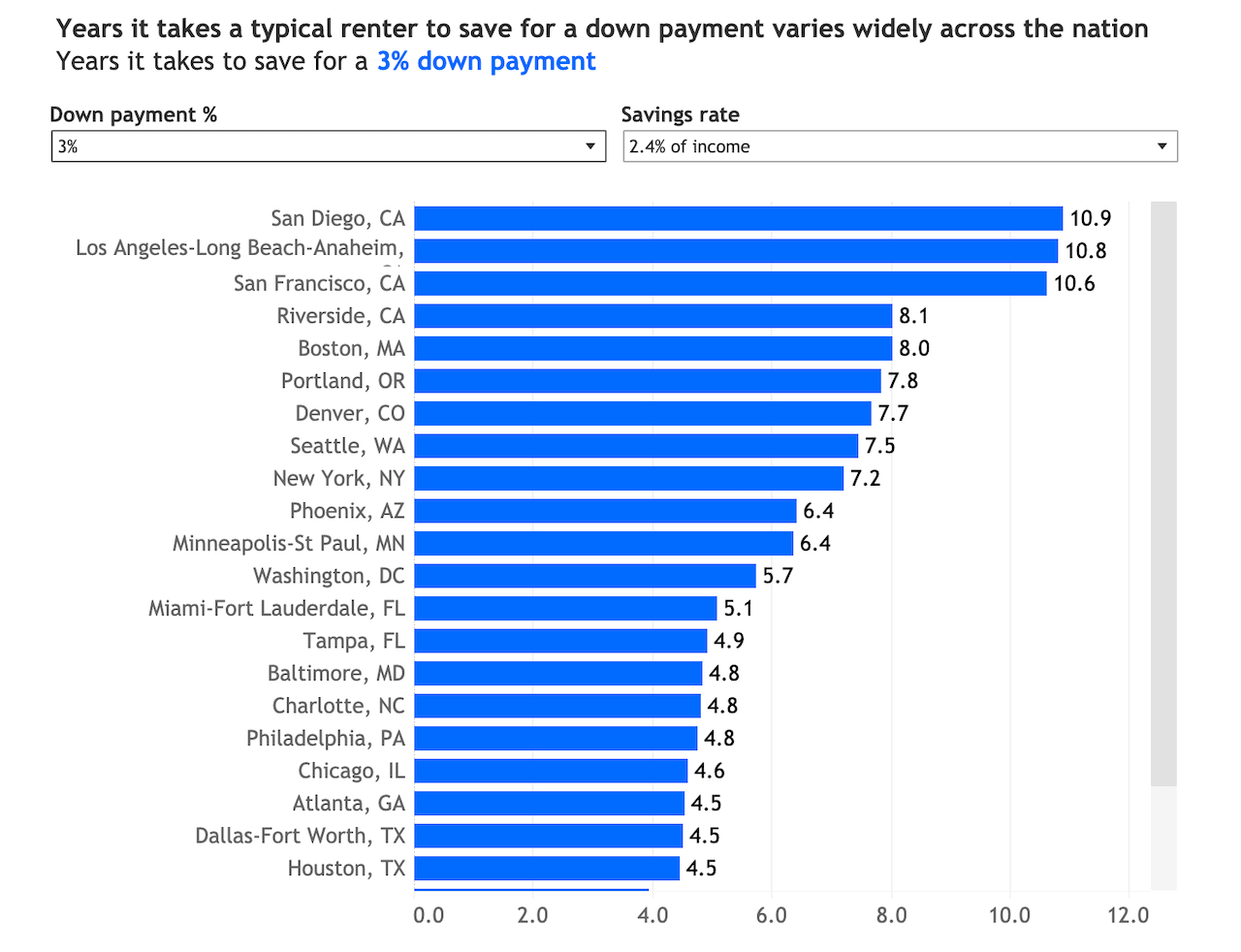

Secondly, have a look at this Zillow research piece by economic data analyst Nicole Bachaud on what – and how long – it takes typical renters to save for a down payment to buy a home.

Roughly two-thirds (64%) of first-time buyers put less than 20% down on their first home, according to the 2020 Zillow Group Consumer Housing Trends Report, and a quarter put down 5% or less. Less than half of first time buyers said they saved the majority of their down payments themselves, meaning the rest used alternate means including gifts and loans from family and friends or tapping into retirement accounts and investments to come up with their down payments. But not everybody has those opportunities. Black and Latinx home buyers were more likely to say they saved at least some portion of their down payments themselves compared to white home buyers, illustrating some of the disparities in how households are saving up for their American dream.

Saving is really the only option for those first-time buyers without the luxury of relying on gifts and investments for a down payment, and it’s becoming increasingly more difficult as home prices soar. For renters making the median U.S. renter income (as of March 2021) of $3,855 per month and putting 2.4% of their income into savings (the median rate for renters), it will take a whopping 26.8 years to save for a 20% down payment on today’s typical starter home, priced at $148,527. That number seems high, and it is — but the good news is that 20% isn’t required. The down payment on most conventional loans can be as low as 3%, bridging the time needed to save for an adequate down payment on a typical entry-level home under the same assumptions down to just down to 4 years.

The issue here is how much of new homebuilders' product and community mix – which has shifted bigtime in the past five years or so – exposes itself to Federal Housing Administration mortgage limits to try to position product to first-time buyers.

What's happened with recent input price inflation, surging land costs, and spiralling local regulatory burden, is that builders in some markets that had up to now enjoyed headroom between their product pricing and FHA loan limitations are increasingly at risk of breaking through those caps.

Whether or not it's the demand pool that's taking a pause – or builders, and whether or not it's tilting toward time for concessions to keep sales per month per community pace where it needs to be remain uncertain.

That's why the Summer of '21 feels like a too-hot blanket right now, and why the one metric builders really don't want to have to begin keeping an eye on is cancelation rates.