Capital

Here's A Look At The $338M New Home-Apollo Deal, And What It Means

TBD's exclusive analysis of a homebuilder M&A transaction that bears not just on the future of one of the industry's premium operators, but on what happens next in a business environment shrouded in uncertainty.

Executives of The New Home Company announced Friday they've agreed to sell the 12-year old, regional company to a financial acquirer – funds managed by affiliates of Apollo Global Management – in an all-cash transaction for $9 per share.

If things go as planned, after Apollo follows a two-step tender offer for shares of the enterprise, the deal is set to close sometime before year-end.

Then, The New Home Company, which has prided itself since going public in 2014 as having principles, values, character, behavior, and culture more like privately-run and capitalized homebuilding operators than public peers, will, once again, be a private, as it was from its 2009 start-up until its late 2013 IPO bid.

And, yet the moment it sheds its ticker symbol NWHM and its shares stop trading on the New York Stock Exchange, the irony of becoming a holding of the $461 billion Apollo global investment empire – $36.5 billion of which are in real assets like real estate – will clarify. Then, The New Home Company will be a privately held, four-market regional homebuilder that acts – in financial performance, investment strategy, and management disciplines – more like a public than most privately held peers.

The deal, for a small-cap public homebuilding enterprise whose customers, employee associates, investors, and submarket and masterplanned community partners mostly view NWHM as an exception to the rules that govern both most publics and privates, comes with an array of telltales, both within its own framework and for the wider sector of market-rate single-family real estate development and construction.

Here's a statement on the combination:

“Over the last several years, we have transformed the company into a growing and diversified builder with operations in three states,” said H. Lawrence Webb, Executive Chairman of The New Home Company Board of Directors [in a press statement]. “We have strengthened our balance sheet, streamlined our cost structure and repositioned our product offerings to cater to a deeper pool of buyers. Apollo’s ability to provide flexible capital and deep knowledge of the homebuilding industry will help us to accelerate the growth of our business. Following a thorough review of the opportunities available to the Company, The New Home Company Board of Directors unanimously determined that entering into this agreement is the best path forward to maximize value for shareholders.”

[Disclosure: Larry Webb – a longtime source and professional friend, is also a TBD Dream Team member, who serves as an occasional source of industry advice].

First, a look at the specific seller and buyer context, and then will take a look at want it means and why it matters as one of a series of M&A deals that have emerged in a time-period – 2020 through 2025 or beyond – defined not just by the Covid pandemic, but by demographic inflection across generational cohorts, household types, and by structural grinding of the wheels of livelihood, household earnings, and the future of work.

The Apollo-NWHM transaction context first.

- The $9 per share price – a premium of 85% to NWHM's July 22 closing share price and a 51% premium to the trailing 90-day volume-weighted average price – valued the enterprise as $338 million, just under 10X EBITDA of $39 million.

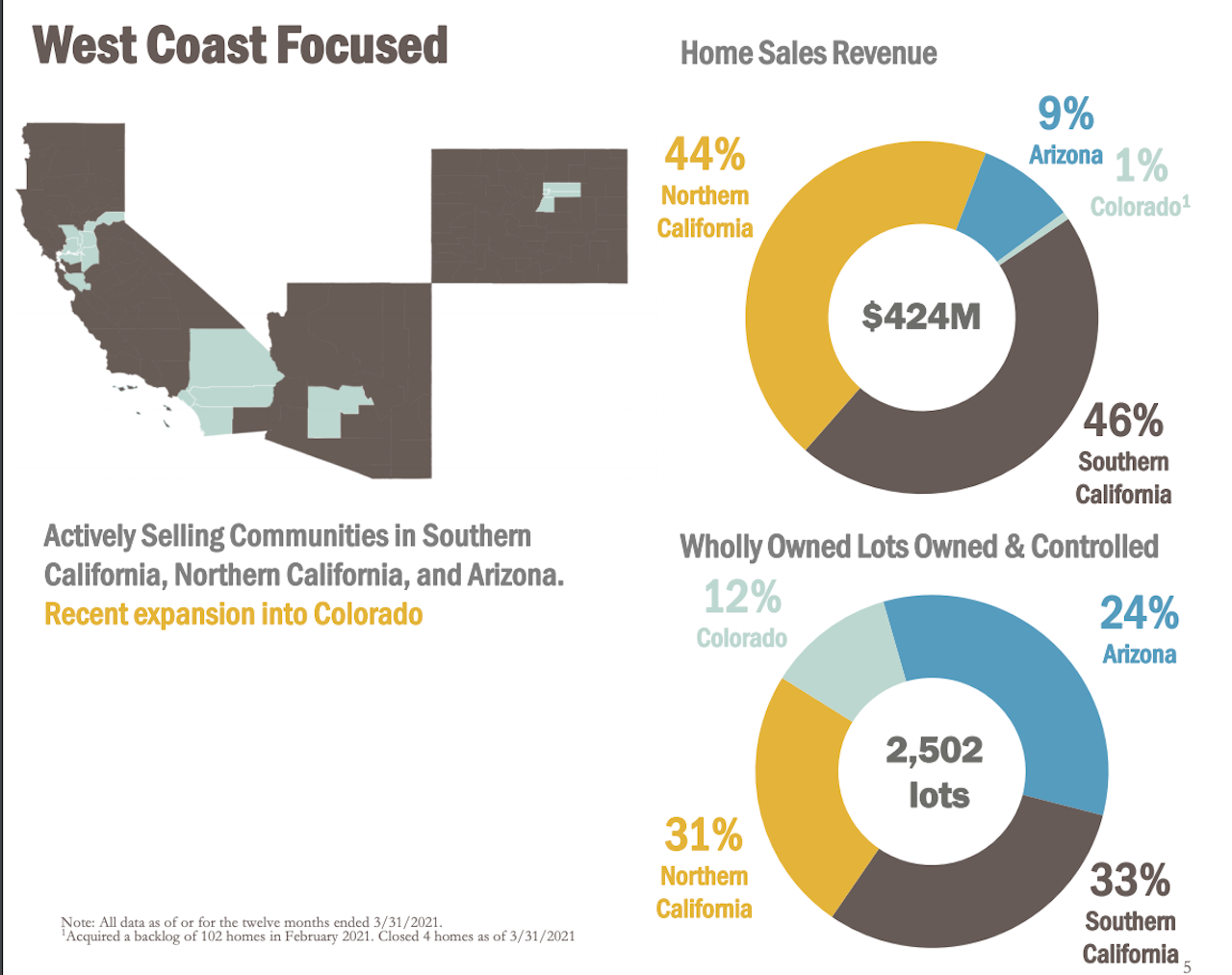

- Here's a look through a different lens, the real estate asset: A $338 million enterprise value would clock in NWHM's 2,500-plus owned and controlled lots at a per homesite current range of about $135,000. Over 61% of the company's owned and controlled lot pipeline is in difficult-to-develop Northern and Southern California parcels and masterplans, driving $9 out of every $10 of revenue the company generates. Arizona (24% of NWHM lots) and newly acquired Colorado (a backlog of 102 homes and just under 300 lots) account for 10% of projected 2021 revenues. The $135k per lot value – spread across not just hyper-expensive California coastal communities but into Arizona and Colorado – gives perspective on how much value NWHM creates to reach its $714,000 average selling price across both ends of its pricing barbell, luxury and entry level.

- The "win" for The New Home Company as seller is three-fold. One, the enterprise valuation at 10X EBITDA, which recognizes value well beyond the physical real estate pricing and reflects brand and operational premiums; secondly, the company – by taking itself private – will no longer bear the costs, reporting constraints, and Wall Street market volatility of a publicly-traded entity; and third, the capital resource depth and expertise of Apollo gives an "outlier" in positioning, branding, and customer and team-member focus an adrenaline burst of wherewithal in an ever-more-competitive land acquisition arena.

- For the buyer, The New Home Company brand, business model, and talent- and customer-positioning gives Apollo an operational, geographic, community development and brand equity platform in the U.S.'s western region that other active investment players would covet, as well as an exclusive opportunity to drive its investment returns. Apollo is not only buying into a land position beachhead in acquiring NWHM, but a clearly defined and differentiated real estate investment capability and customer value proposition model that aligns with its broader real estate investment program.

- Too, the buyer may see opportunity to release value and profit-generating capability in the company that the Street may not currently – nor in the future – appreciate nor accord the company, both by applying its own operational and management skill-sets, and freeing The New Home Company model of encumbrances to be bolder and go bigger in its mission.

“I am extremely proud of our team and the progress we’ve made over the last few years in transforming the company into a more profitable, better positioned homebuilder,” said Leonard Miller, President & Chief Executive Officer of New Home [in a press statement]. “We are excited to enter into this new chapter together with Apollo, who shares our strategic vision for New Home as a platform for delivering quality homes and communities with award-winning design and unparalleled customer experience. By joining forces with Apollo, we will have the financial flexibility to build on our recent successes and take the company to new heights.”

The macro real estate and homebuilding and development backdrop for merger, acquisition, and "financial event" activity in 2021 to date, and the back half of 2021 into and beyond 2022 coalesces around several once-in-a-generation force factors that accompany an array of relatively normal – if unpredictable – cyclical tides.

- The Pandemic Disruption to a more normalized, stabilized, unaided economic cycle: The gigantic and unprecedented series of offsets – economic apocalypse to economic and financial rescue to economic recovery to economic equilibrium without intervention – intensifies risk-reward scenarios for the foreseeable, forecastable future.

- The Millennial moment – an age-defined juggernaut cohort that has only just begun to release its collective impact on household formation and economic performance – may sustain an altered state of consumption on the housing and consumer spending front for several years to come.

- An accommodative Fed: Despite indications that the Federal Reserve may have to accelerate its plans to taper its purchase of bonds, and, even potentially, begin ratcheting up its prime lending rates, expectations remain in place that the U.S. Central Bank will keep support of housing and economic activity as fully flowing as it takes to drive unemployment toward full employment. This should put a long-term lid on capital costs, which pushes investment farther forward into the future.

- The proliferation of company sellers. Age demographics on the owner, founder, principal front has drawn more belles to the ball, as succession plans, earn outs, estate plans, personal loan guarantees all factor into why a potential operator may have an especially attentive ear to the ground on potential opportunities to sell.

- The super-charging of potential buyers. Developed, vacant lot land scarcity, structural chronic underbuilding, and a dashboard full of demand for housing and historically low costs of capital – all energized by pandemic fear and protectionism as well as time-delayed biological clocks – have entities teaming into the havens of single-family residential construction as one of few places for a crush of liquidity. Strategic homebuilders, global homebuilding companies from Asia, Canada, even South America, mega-manufactured housing player – Clayton – and, recently, a host of institutional capital investment blue chip names have become active suitors, trolling for local, regional, and multi-regional homebuilders and their ecosystem of business partner and homebuyer customer relationships.

For the reason that both potential sellers and potential buyers can be intensely motivated owing to particulars of their individual cases, a welter of deal conversations, letters of intent, and agreements is likely, all due to a single, overriding fact.

There's too little new housing; and too much demand for it. But, that supply-demand reality doesn't mean every bet on land will pay, for every bet has its own local realities and its own set of timing factors that make it a win or a lose.

For The New Home Company, the timing was right for it to pivot from being the public company that acted in most ways like a private, to being a private company whose professional financial disciplines make it feel in important ways like a public.

Join the conversation

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Capital

Timing Demand: Why Investors Choose To Buy Apartments Vs. Building

A construction slowdown today is setting up an undersupply tomorrow. Opportunistic, patient investors are already pivoting to seize future market growth catalysts.

Little Deal ... Big, Timely Product Pivot: Lokal’s Capital Play

A $12M facility fuels Lokal Homes’ swift shift into higher-margin homes and a smarter land strategy in a tough market.

Land, Capital, And Control — A New Playbook In Homebuilding

Five Point Holdings’ acquisition of a controlling stake in Hearthstone points to the direction of homebuilding strategy: toward lighter land positions, more agile capital flows, and a far more disciplined focus on vertical construction, consumer targeting, and time-to-market velocity.