Capital

The Demand Debate: Who's Down For The Real Count?

Why are household formation rates falling? Here's five vital statistics in structural demand builders can not afford to ignore.

Gloves are off in new residential construction's great demand debate.

The stakes in the game could hardly be more intense. The context here is tens of billions of dollars of investment capital hellbent on yield, and little opportunity so alluring – globally speaking -- as residential real estate and its enormous mismatch between a tsunami of younger-adult households in the making and the inadequate number, quality, location, and attainability of homes and communities to shelter them.

Demand – structural, fundamental, demographically-driven, and sustaining – stood as the "given" developers, builders, investors, and their myriad partners could count on whatever transitory headwinds might kick up in a moody economic backdrop.

Which door do you pick?

- Door No. 1: The National Association of Realtors, based on research by the Rosen Group, estimates a current "underbuilt" level-set at 5.5 million homes.

- Door No. 2: Freddie Mac research calculated a deficit of 3.8 million homes in 2020.

- Door No. 3: National Association of Homebuilders analysis, tracking housing vacant units and vacancy rates, tops out at about 1 million as a working proxy for undersupply.

- Door No. 4: Forget all of that. At current production levels, developers and builders are currently oversupplying the market, with financial consequences to come sooner or later.

In what world of upended markets and parallel realities could we go from being underbuilt by 5.5 million to a current single- and multifamily starts pace that not only exceeds pent-up demand but soon will clock in as a glut by 200,000 or 300,000 or more new homes beyond what the national market can absorb?

A good person to ask, for a sound, clearly evidence-based, assumption-by-assumption construct of past, current, and future housing demand versus past, current, and planned supply is John Burns, ceo of eponymous housing analytics and advisory firm John Burns Real Estate Consulting.

Here's a hint at his take on the math. Tweets Burns:

We are under building for today's demand surge, but building more than our long-term need of 1.4 million homes/year that we forecast in our book Big Shifts Ahead 5 years ago."

Earlier, contrary to wider-held assertions that soaring house prices served as evidence of massive national undersupply in the context of population growth, atypically low vacancy rates, and economic headway, Burns offered this reality check:

Our adult population isn’t growing as fast as it used to,” said Mr. Burns, chief executive of John Burns Real Estate Consulting LLC. Compared with decades before 2000, “we don’t need to build as much,” he said.

What builders do with that – not just insofar as their efforts to lean into the surge right now, and deliver up as much and as often as they can to keep pace, but in the calculus of their time-released investments in land for later – is critical.

Underlying the red-flag, still contrarian view the Burns team at JBREC embraces are the raw material inputs of any business-to-consumer market outlook.

Household demographics.

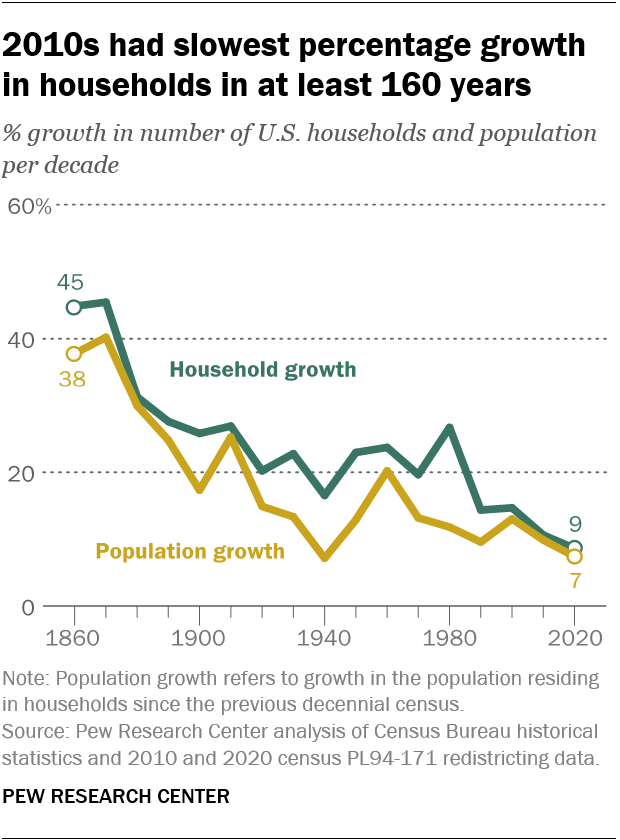

Fact is, household demographics crossed an inflection point that coincided with the Great Recession. Here's the way Pew Research analysts Richard Fry, Jeffrey S. Passel, and D'Vera Cohn describe the tipping point:

Growth in the number of U.S. households during the 2010s slowed to its lowest pace in history, according to a Pew Research Center analysis of newly released 2020 census data.

The 2020 census counted 126.8 million occupied households, representing 9% growth over the 116.7 million households counted in the 2010 census. That single-digit growth was more anemic than the prior record low percentage growth of households (11%) during the previous decade, as shown in the 2010 census.

Three Vital Statistics For Housing

What this means for the U.S. economy may not be fully appreciated. Households, we know, fuel a full one-third of Gross Domestic Product economic activity. They're the engines of the nation's outlook, directly impacting residential real estate investment, development, and construction, and indirectly exerting multiplier-effect force on countless related local, regional, and national business fortunes.

Pew research analysts flag three underlying trends currently resculpting the landscape of household formation, equally material for stakeholders in homebuilding and development.

- The rate of population growth – a core ingredient of household formation – slowed during the same period to 7%, the lowest rate since the 1930s.

- Multigenerational households increase – a spike from 12% multigenerational households in 1980, to 20% in 2016 – mutes household formation rates.

- Further, faster population growth among race and ethnicity groups less likely to form households:

Asian and Hispanic adults – the fastest growing racial or ethnic groups in the U.S. – are less likely than White and Black adults to live in separate households. In 2020, there were 42.2 households for every 100 Hispanic adults and 41.9 households for every 100 Asian adults.

Finally, of real importance in where housing demand is headed, a tipping point, the rate at which adults live in their own household fell.

Overall, the household formation rate declined slightly from 51.5 households per 100 adults in 2010 to 50.9 households per 100 adults in 2020.

Geographic, occupational, and financial reasons also play into why household formation rates reflect a diminishing return.

The nature of housing demand itself – an equation that in reality blends wherewithal in a livelihood sense with lifestage with housing preference – may be entering a transitional, transformational era.

The limbo of the future of work and the future of home may define who's long on land right now and who's not.

Join the conversation

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Capital

Timing Demand: Why Investors Choose To Buy Apartments Vs. Building

A construction slowdown today is setting up an undersupply tomorrow. Opportunistic, patient investors are already pivoting to seize future market growth catalysts.

Little Deal ... Big, Timely Product Pivot: Lokal’s Capital Play

A $12M facility fuels Lokal Homes’ swift shift into higher-margin homes and a smarter land strategy in a tough market.

Land, Capital, And Control — A New Playbook In Homebuilding

Five Point Holdings’ acquisition of a controlling stake in Hearthstone points to the direction of homebuilding strategy: toward lighter land positions, more agile capital flows, and a far more disciplined focus on vertical construction, consumer targeting, and time-to-market velocity.