Marketing & Sales

Bubble? No Bubble? Sometimes You Just Have To Trust Your Gut

By-the-numbers takes a more personal turn, to see the writing on the wall. When there's a disparity between housing economic models and common sense, it may be that the models aren't up to the task.

2008

That’s when I learned, the hard way, what can happen when a housing bubble bursts.

At that time I was the CEO of Hanley Wood, the media company best known at the time for publishing BUILDER magazine. Like most businesses tied to housing the company had been flying high. And why not. Housing starts had not only been strong since 2000, topping 2 million units in 2004 and 2005, but the company had been purchased by a big time private equity firm in 2005.

Beyond that our customers, mostly building product manufacturers, couldn’t buy enough of what we were selling, mostly advertising in our magazines and exhibit space in our trade shows. Moreover our private equity partner was providing us with the capital to acquire or launch more magazines and trade shows and to launch big, expensive digital media products. We also bought our first data business. We couldn’t hire people fast enough.

And it all seemed to be working. The biggest single issue of BUILDER generated more than $2 million in revenue, which was more revenue than the whole company generated in its first year of business in the early 1980s. Between 2000 and the beginning of 2008, the company more than doubled its revenue, tripled and-then-some its earnings, and more than tripled its on-paper valuation.

We had also loaded up on lots and lots of debt.

The housing market had slowed down in 2007, but most economists forecast a soft landing for the housing market with starts just falling to around a still solid 1.5 million units. As I recall we were more pessimistic than that but didn’t see what was coming.

I remember the first sign of real trouble. I was in Chicago and got a call from one of our biggest and best customers. He told me his company had decided to cancel its whole advertising program. Just like that. No discussion, no compromise. Goodbye $1 million.

As news of the subprime mortgage crisis began to spread and housing starts began to plummet, I got more and more of those calls. And when Bear Stearns crashed and burned and the housing bubble burst like an artillery shell and spread deadly shrapnel through the whole economy all I could do was wonder how I hadn’t seen the handwriting on the wall.

Hanley Wood survived the slaughter (it’s now called Zonda) but investors big and small collectively lost hundreds of millions of dollars and hundreds of employees lost their jobs. And I got to spend the last 2 years as CEO of the company talking to bankruptcy attorneys and bankers instead of customers.

Which brings me from then until now. And now I think I can see some frightening handwriting on the wall. It says housing prices are going to fall and take the housing industry down with them.

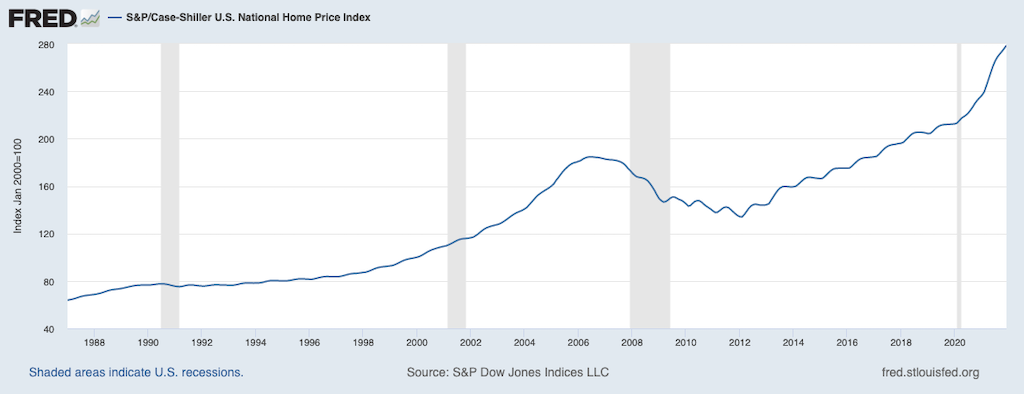

In support of that warning I’m not going to use too many economic statistics, but one statistic does seem worth mentioning. Housing prices have increased 27% in the last 2 years. Pandemic or no pandemic, that seems unsustainable. An adjustment seems inevitable.

But in support of that warning I am going to stick with the personal approach I’ve taken in this column. I own (mostly free of mortgage) 3 houses. One went on the market last week. We thought about selling it last year, and were told it would fetch about $1,100 a square foot. A year later, it listed at $1600 per square foot price. The house sold — at about 3% above asking price — within a few hours. The buyers never visited the house. They took a FaceTime tour with the listing agent.

We bought another house 14 months ago. According to Zillow, it’s already increased in value by 40%. And houses in this market are selling overnight.

We’ve owned the third house for 11 years, and according to Zillow it’s increased in value in the last 2 years by 40%, an estimate supported by experienced local real estate agents.

All of which reminds me of another lesson I’ve learned: Anything that sounds too good to be true, isn’t. Which makes me wonder if builders shouldn’t be worried that the backlog of houses being built but not yet finished is at the highest level since 1974.

Maybe it’s time to slow down … before the bubble bursts.

Join the conversation

ABOUT THE AUTHOR

Former chairman & CEO of Hanley Wood, Frank Anton is one of housing’s iconic voices. Currently, he’s advisor to several housing organizations, and is a member of Harvard’s JCHS Policy Advisory Board.

MORE IN Marketing & Sales

When Homebuyers Pull Back, Builder Brands Must Step Up

In markets under stress, consistency, empathy, and value-driven messaging provide builders with a critical edge among today’s cautious buyers. Advisor Barbara Wray gets real about the path forward for homebuilders today.

What Separates Homebuilders Thriving Amidst 2025’s Chaos

Builders face rising stakes to unify tech, data, and operations or risk falling behind amid affordability, insurance, and labor challenges.

Here's Why Randy Mickle Has Joined Drees At This Moment

The new Southeast Regional President brings big, national builder experience to a multigenerational homebuilder with bold goals for its centennial.