Leadership

Why We See Builders And Buyers As People, Not Abstract Statistics

This is personal ... when economic trends swing wildly and cyclical forces evolving so fast, let's not forget that lives, and livelihoods, and human stories hang in the balance here.

The best and truest part of Peter Coy's New York Times economics opinion column – "The Housing Market Is Bad But Not That Bad" – pops up as a coda, a 1961 quotation from the John Steinbeck novel, The Winter of Our Discontent.

What a frightening thing is the human, a mass of gauges and dials and registers, and we can read only a few and those perhaps not accurately.”

On the other hand, the worst and least true part of this iconic business journalist's housing market observation – in The Builder's Daily's view – comes five paragraphs into the analysis, where Coy writes.

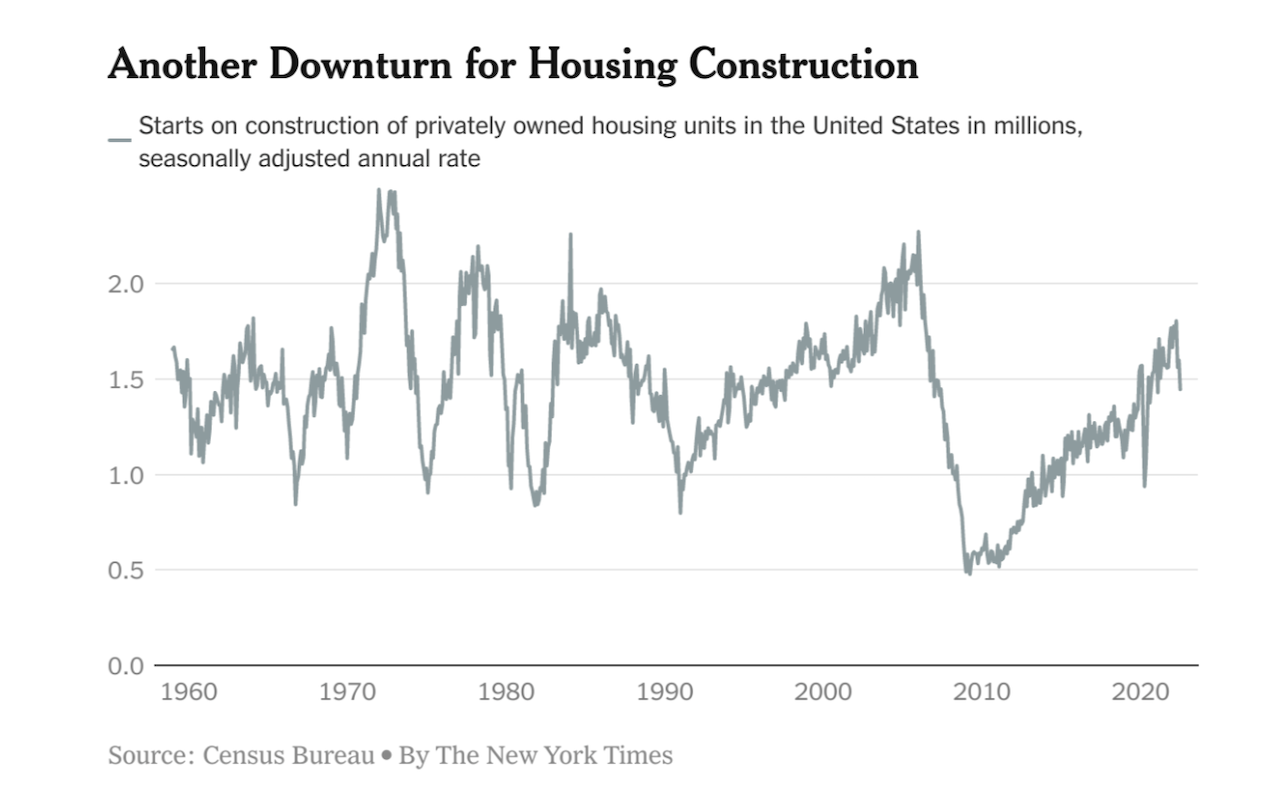

The downturn since the most recent peak in December — the one Ian Shepherdson called “terrible” — is that comparatively small chupchik way over on the right." [See chart below]

Now, without looking up the word chupchik [curiosity got the better of me, and I did], it pretty much sounds like what it means, which is sort of a measure of "meh."

Now, the two reasons we'd take exception to Coy's dismissal of housing's downward trajectory, as a "small chupchik" are these:

- All you have to do is go back to the other four housing cycle peaks – shown on the chart during the early and late 1970s, the 1980s, and in 2007 or so – and imagine the "early innings" months just past each of those peaks. With the same framing bias, Coy would have written off each of those post-peak inflection periods as a "small chupchik," i.e. way better than "terrible." Seems premature, by historical measures, to call that sharp, knife-edge fall-off since Jan. 2022 a chump-change no big deal.

- The other reason – and the one that causes us to say that the remark is the "least true" in Coy's analysis – is the profoundly dehumanizing take-away on the cause-and-effect nature of the Federal Reserve's monetary and fiscal policy tack.

Coy writes:

The Fed is trying to squelch inflation by cooling off economic growth, and one of the most effective ways to do that — as I wrote on Monday — is to put the squeeze on housing construction. Builders and buyers alike step back when interest rates rise.

"Builders and buyers," however they're referred to in this analysis, are inanimate economic behavior quantities. They're real people.

Those same buyers who "step back" because both qualifying for and handling monthly payments for principal and interest payments suddenly don't match up to their household budgets don't only lose now. They're also bound to take a hit later -- when the Fed backtracks toward stimulus and interest rates come back to within their means – because they're going to be returning to an even more dramatically undersupplied market.

These "buyers" are not solely statistics. They're families, workers, households whose ability to evolve financially and settle in towns and cities makes those places dynamic economic centers. They don't "step back" and "step forward" mechanically. They strive. They battle challenges. They become us.

Nor is the broad-brush comment, "builders step back when interest rates rise." It is a falsehood to conflate an outcome – fewer housing starts – with most homebuilders' sense of agency here. Starting fewer homes because a) the lifeline of homebuyer revenue is showing signs of distress, and b) the lifeline of forward-looking capital lending is increasingly at risk can't be described as "stepping back."

For homebuilders – the people, not the faceless corporate entities, or an abstract business sector – I've known across two decades, "stepping back" is not part of the vocabulary. In any given calendar year, or three years, or two weeks, they're already in too far – in front-loading use of acquisition, development, and construction project and entity lending and investment -- to literally, "step back."

Stepping back is a mischaracterization of homebuilders "choice" here. If they're choked off from essential revenue and capital, they're not stepping back.

And when builders are choked off from those lifelines of homebuyer revenue and new capital, the economic impact is not abstract either it's real.

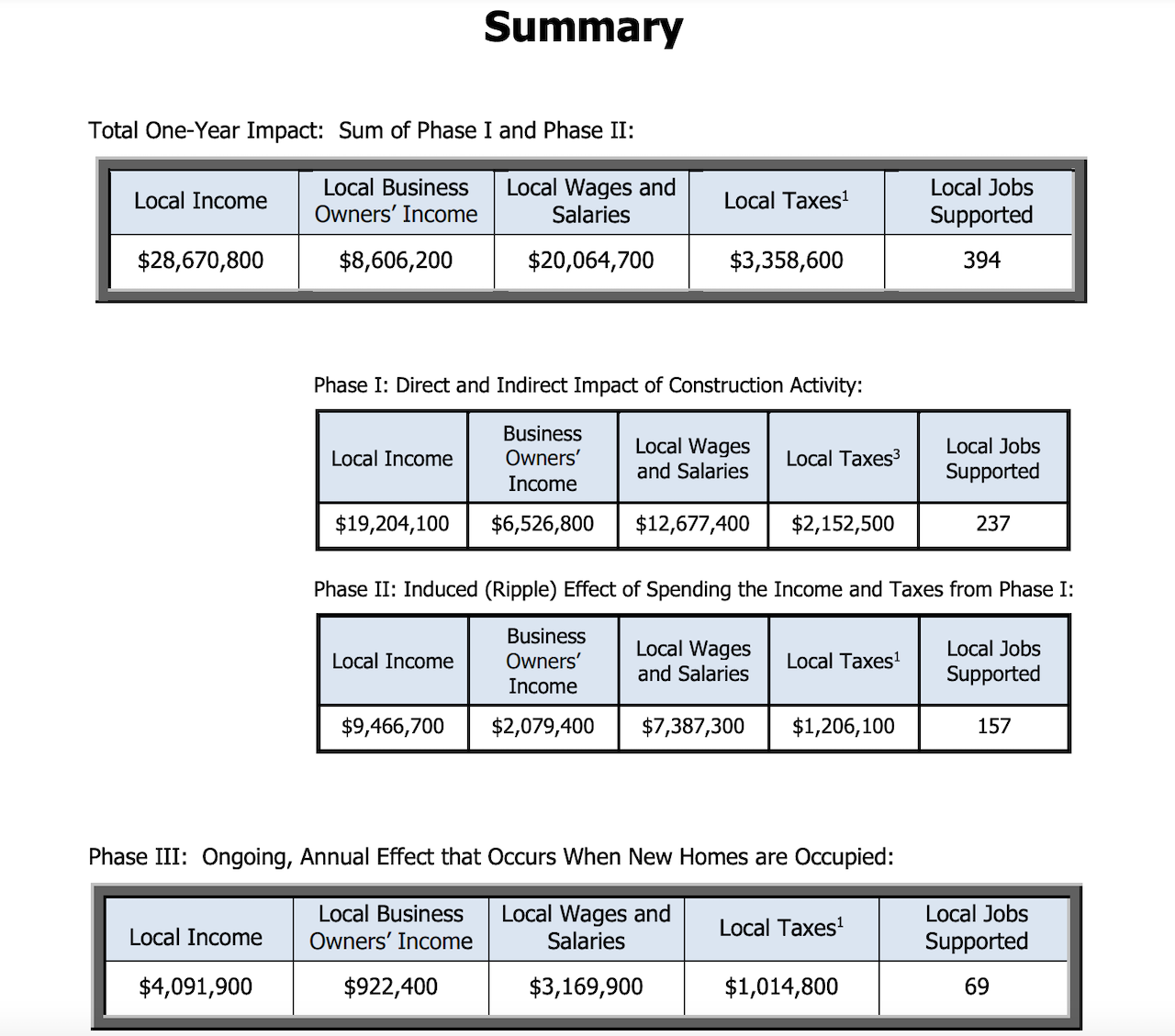

A 2015 analysis – updated here in 2020 -- from the National Association of Home Builders, calculates multiplier economic impacts of new residential development and construction. Here are some of the topline data points of that study.

Impact of building 100 new homes

The estimated one-year impacts of building 100 single-family homes in a typical local area include

- $28.7 million in local income

- $3.6 million in taxes and other revenue for local governments, and 394 local jobs.

The additional, annually recurring impacts of building 100 single-family homes in a typical local area include

- $4.1 million in local income,

- $1.0 million in taxes and other revenue for local governments, and 69 local jobs

Here's how those multiplier effects chart out:

The 2020 update to this analysis illustrates the job creation and tax generation impacts of each completed single-family home here:

- Building an average single-family home: 2.90 jobs, $129,647 in taxes

This data – economic modeling though it may be – may help to put human faces and human striving and human contribution to statistical impacts we're seeing occur within the compass of homebuilding and its related business ecosystem.

Let's take stock of what Coy himself writes in his conclusion that "The Housing Market Is Bad, But Not That Bad."

There’s a short-term cycle effect and then a long-term issue of how much housing we need,” Robert Dietz, the chief economist of the National Association of Home Builders, told me. “For the longer term, are we overbuilt? I have to still answer no.” What’s more, he said, banks have lent more judiciously this time than in the housing bubble, so there’s been less nonsensical construction.

Taking into account both short- and long-term factors, he’s forecasting a drop of at least 10 percent in construction of single-family homes this year, the first calendar-year decline since 2011. That’s bad, he says, but not nearly as bad as the plunge after the real estate bubble began to burst 16 years ago.

If Dietz is now correct in his estimation that single-family housing starts may be on pace to fall below the 1 million mark, that would reflect a net variance – versus an earlier 2022 forecast published by Bill McBride of Calculated Risk – of 113,000 homes or more, not started in 2022.

{kind=link}

So when you look carefully at what "not that bad" adds up to in terms of some of the impacts on people of homebuilders starting 113,000 fewer homes in 2022, the calculus quickly spools up into the trillions of dollars and tens of thousands of livelihoods, hitting both within the 12 months of the starts themselves, and the aftereffects of those missing new homes.

When you really boil it down to the human level, even a 10% decline – which we believe will wind up being a conservative estimate – deserves more than mention as a "chupchik."

Join the conversation

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Leadership

Westwood-Hippo Deal Raises Stakes On Home Insurance Trust

A landmark deal expands embedded insurance capabilities, aiming to ease closings, manage climate risk, and restore buyer trust.

From Afterthought to Dealbreaker: Why Home Insurance is Now Key to Sales

By working with the right insurance expert, builders gain short- and long-term advantages in keeping current deals on track and making sure their business thrives into the future.

How Outlier Homebuilders Build An Edge, Even In a Slow Market

Focus On Excellence 2025 reveals what top homebuilding leaders are doing now to separate—and stay ahead—for 2026-through-2030 and beyond.