Leadership

Millennial And GenZ Buyers Drive 60% Of Home Purchases

Here’s how homebuilders and their partners team up to solve for both the math and the psychological challenges with tech when digital natives want it, and people when they need them.

Westwood Insurance Agency

Leadership

Millennial And GenZ Buyers Drive 60% Of Home Purchases

Here’s how homebuilders and their partners team up to solve for both the math and the psychological challenges with tech when digital natives want it, and people when they need them.

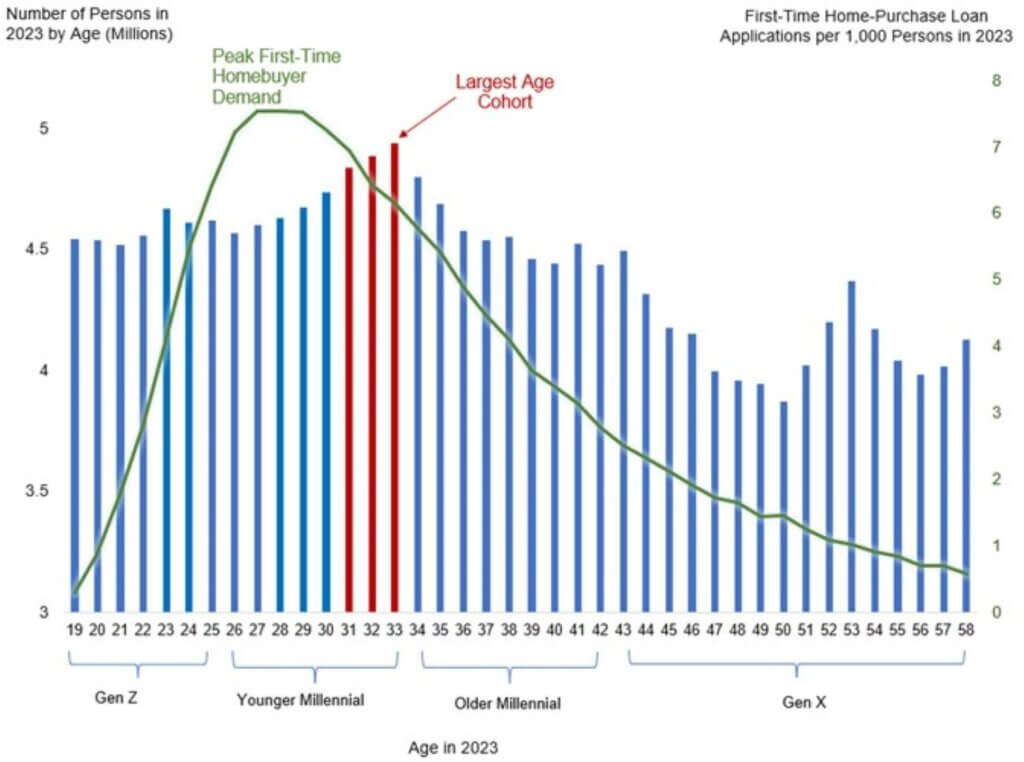

Millennials and a leading edge of Generation Z young adult households – the generational heart and soul of a burgeoning pivot to a digital native consumer America – together make up three out of every five home purchase mortgage applications in today’s housing market, especially among first-time homebuyers.

Their two-pronged impact on overall housing demand can scarcely be overstated, as this commentary from Core Logic illustrates.

The share of millennial first-time homebuyer (FTHB) mortgage applications is even higher than that of overall home purchase applications for that generation, a figure that comprises both FTHBs and repeat buyers. Millennials accounted for about 68% of all FTHB home purchase applications in 2023, a pattern that is not surprising, as the largest portion of this generation has approached the peak age of typical FTHBs.

Gen Z, the youngest homebuying group, accounted for 15% of FTHB purchase applications in 2023, up by 5 percentage points from 2022. This share is likely to increase in the coming years.”

Further, these two demographic forces have staying power as demand drivers – particularly for new home construction. As Core Logic notes, “millennial homebuyer demand is likely to remain strong over the coming years,” providing macro employment, earnings, and economic trends continue to show fundamental strength, while a significant amount of existing home stock sits “locked-in” with owners unwilling to trade out of historically low mortgage interest rates.

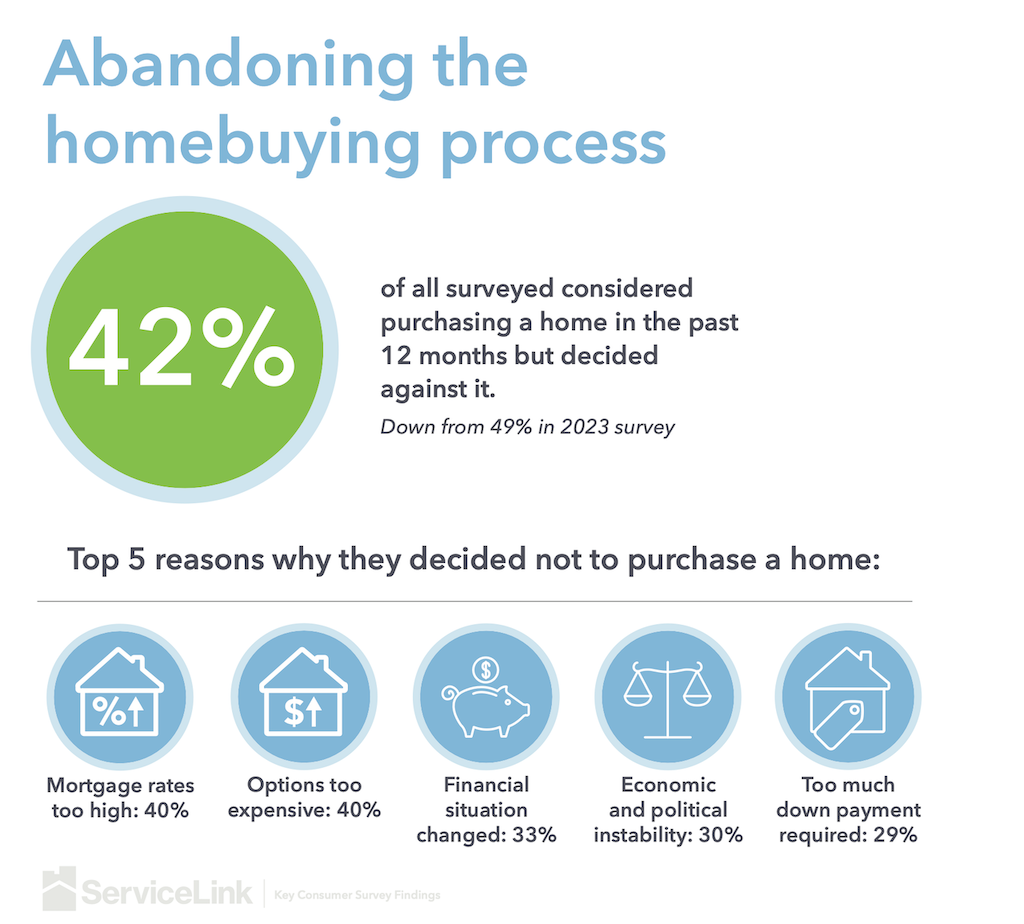

What’s clear from the data is that Millennial and GenZ adults report that they’re the most motivated and “eager” generations of all to become homeowners. What’s equally clear is that affordability – particularly as a tricky and volatile moving-target matter – is a challenge acute enough to cause more than two out of every five would-be homebuyers to abandon their purchase journey before they reach closing.

Fresh data from the National Association of Home Builders – citing the impacts of both selling price increases and hikes in 30-year fixed-rate mortgages – suggests that 103.5 million households, or 76.9% of all U.S. households, are “already not able to afford a median-priced new home ($495,750).”

A recent report from Redfin notes that a household looking to afford a typical U.S. starter home now needs to earn $75,849 annually, up 8.2% (an increase of $5,767) from the same time in 2023:

The income necessary to buy starter homes is increasing from a year ago due to rising prices and mortgage rates: The typical starter home sold for $240,000 in February, up 3.4% year over year, and the average 30-year fixed mortgage rate was 6.78%, up from 6.26% a year earlier.”

Homebuilders and their business partners have navigated both financial and psychological challenges to keep buyer engagement and sales absorptions at better-than-expected closing rates with an agile array of case-specific value-adds, incentives, and mortgage buydown opportunities designed to price them in, not out.

Two factors make it extra challenging for younger buyers,” says Amanda Taylor, Vice President of Communications and Marketing at Westwood Insurance Agency. “One is, by definition, a first-time buyer doesn’t have a home they’re selling, so there’s no wealth effect from home appreciation over the past five-ish years they can tap into right now. The second challenge is that most of them are still dealing with significant student debt. Around 40% of millennials have sizable student debt, so when you're making that payment each month, it takes away from what could go to your mortgage or your insurance.”

Taylor explains that Westwood works to mitigate these challenges by doing the insurance shopping legwork for them.

It's that slate of 40-plus insurance companies with whom we work, and home insurance policies that are designed for new construction homes to be able to maximize discounts for these would-be buyers,” Taylor says. “We see an average savings of $200 a year, and that can make all the difference to get to closing.”

Moreover, constantly-changing mortgage rates and home price increases have now been joined by rising rates and harder-to-find home insurance as a moving-target factor that can impact both monthly payments and the ability to close on a mortgage. The emotional rollercoaster for buyers has become nearly as important an obstacle as the ability to make a sufficient down payment and meet monthly payment obligations.

With a lot of first timers in the market, buying a house is complicated. It's emotional,” says Westwood’s Taylor. “It's stressful, and that stress on the homebuyer in turn puts a lot of pressure on the new home sales consultant, the loan officer, and the insurance agent who face the challenge of explaining the process to first-time homebuyers. What we find works well for digital native Millennial and GenZ first-time buyers is what we refer to as ‘technology when you want it, but people when you need them.’”

Taylor explains that Westwood agents spend time with new homebuyers starting early on in their journey, talking them through their policies, doing a policy and coverage review and delving into all the details. This way, a buyer can feel comfortable that they have the right level of protection for their needs, and they’re clear on what's included in home insurance and what's not included in the event they may need to supplement it, for example, with either flood insurance or extra personal property protection.

We find that – perhaps surprisingly for such young tech-oriented generations – they do want to talk to someone to be educated on the process.”

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Leadership

How Signature Homes Wins While Other Builders Pull Back

Sales are sliding for most private builders. Dwight Sandlin’s team is defying the trend with strategy, speed, and customer obsession.

HW Media Acquires The Builder’s Daily, Expanding into the Homebuilding Vertical

Strategic acquisition adds leading homebuilding publication and strengthens HW Media’s commitment to serving the full housing economy

C-Suite Leaders Will Gather To Chart Homebuilding’s '26 Reset

The Builder’s Daily announces the speaker lineup for this October’s high-impact leadership summit in Denver, where the best minds in homebuilding operations, marketing, and technology will explore how to lead through the now and build for what’s next.