Land

A Framework for Overcoming Housing’s Greatest Challenge

SLC Advisors' Scott Cox proposes a way homebuilders -- public and private -- might navigate a crossroads of big challenges and long-term opportunities.

The U.S. residential real estate development and construction industry stands at a crossroads. Five macro challenges — profound affordability mismatches, macroeconomic turbulence, local opposition to development, climate-related risks, and labor/technology shifts — converge to create a landscape of profound uncertainty. Yet, within this complexity lies a resilient optimism driven by the demographic wave of Millennials and Gen Z entering homeownership and Baby Boomers seeking their forever homes.

This confluence of challenges and opportunities sets the stage for a critical moment of reflection and action. The insights The Builder's Daily Dream Team contributor Scott Cox, founder and principal of SLC Advisors, shared at the ULI 2024 Fall Meeting offer a timely and pragmatic lens through which industry leaders can chart a course forward. His analysis, rooted in data and practical solutions, cuts through the noise to highlight actionable strategies for the sector.

Critical Insights from Scott Cox: A Pragmatic Path Forward

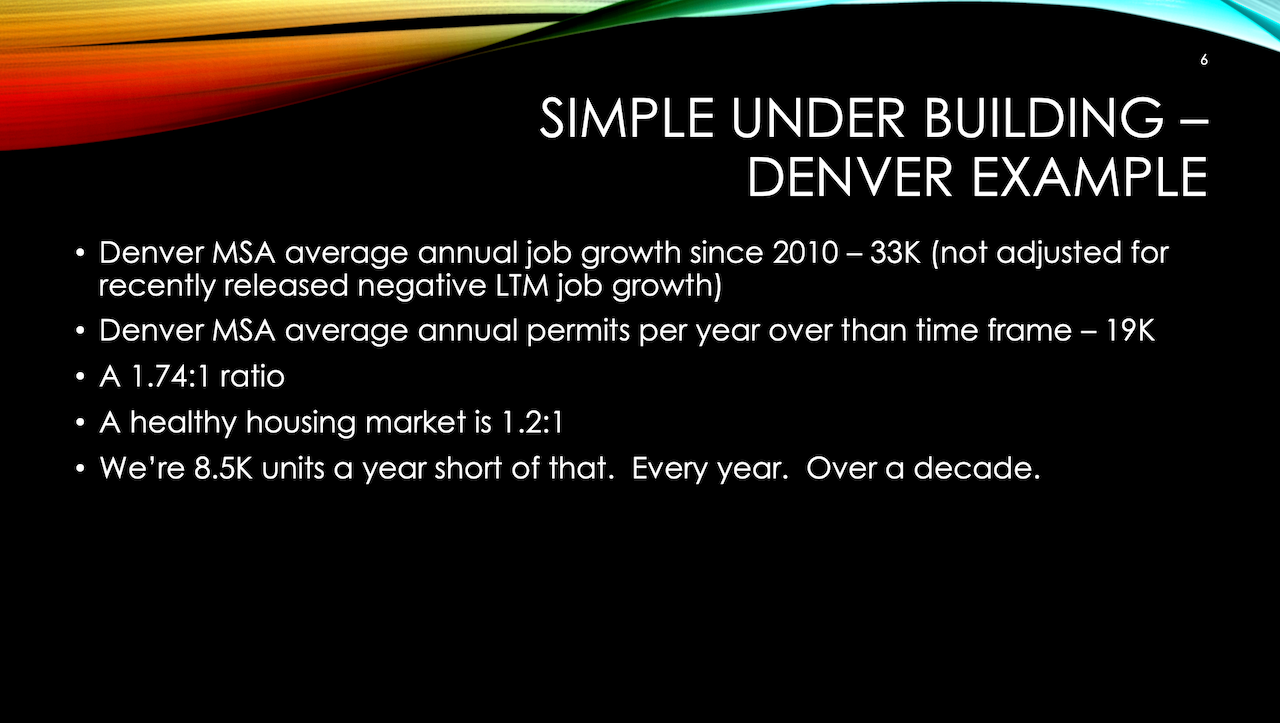

Affordability and Underbuilding: A Persistent Gap

Scott Cox emphasizes that the housing affordability crisis is not the result of a market failure but a failure in land use policy, compounded by political inertia. Using Denver as a case study, he reveals the stark gap between job growth and housing permits.

- Key Stat: Denver MSA has averaged 33,000 new jobs annually since 2010 but only 19,000 housing permits — a 1.74:1 ratio, far from the healthy market benchmark of 1.2:1.

- This shortfall means Denver is 8,500 housing units behind each year, or 85,000 units over the past decade, creating a compounding housing deficit that drives prices skyward.

- Takeaway:

Every year, we fall 8,500 units short. Over a decade, that’s 85,000 homes—a hole too deep to fill without structural change.”

- Leaders must advocate for policy shifts to enable the development of more housing at a faster pace. Without such changes, the gap will continue to grow, further eroding affordability.

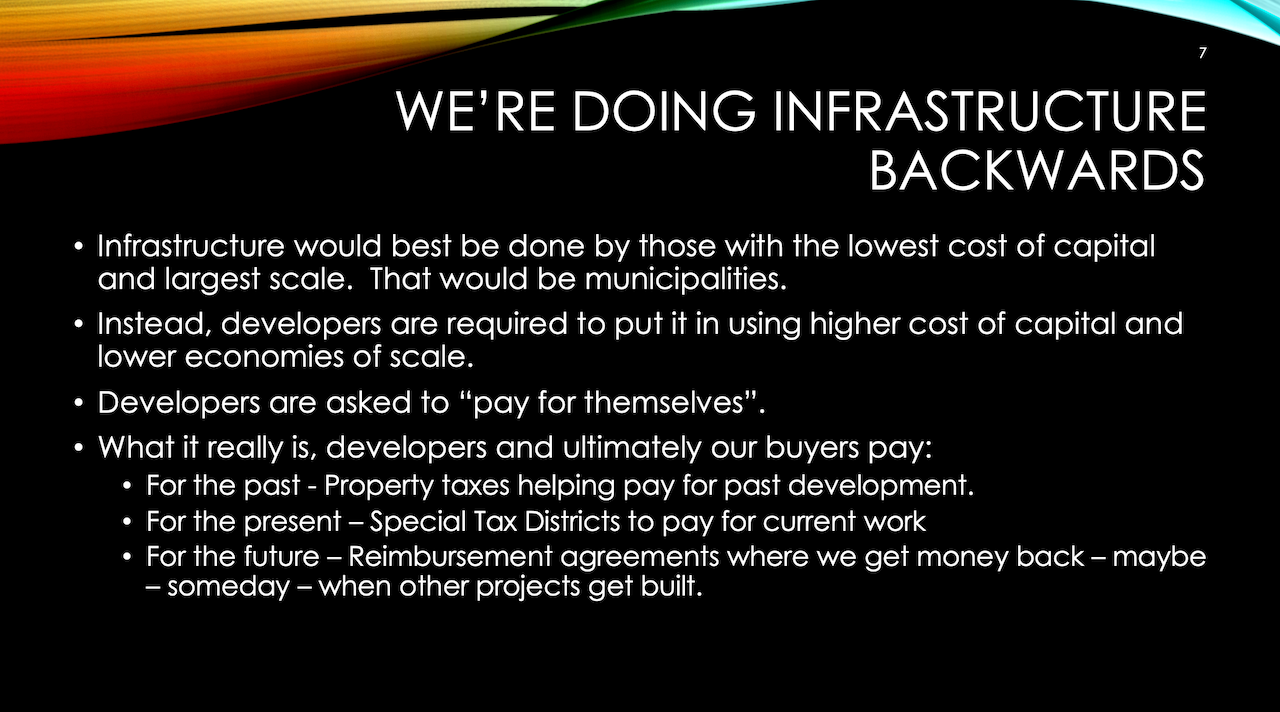

Infrastructure and Financing: Misaligned Incentives

Cox critiques the fragmented approach to infrastructure financing, where municipalities offload costs onto developers, who in turn pass them to buyers.

- Insight: Developers are required to shoulder costs for infrastructure that municipalities should ideally fund.

- This approach inflates housing prices as developers use higher-cost capital than municipalities would. Buyers, in turn, bear these costs through elevated property taxes, special assessments, and future reimbursement agreements.

- Example: Homebuyers pay for new infrastructure and subsidize the costs of past developments and future expansions.

- Impact: This structure disproportionately inflates housing costs and slows the pace of development. It reduces the efficiency of housing delivery and deters smaller-scale developers who lack the financial capacity to navigate these burdens.

- Call to Action: Advocacy for municipalities to prioritize infrastructure investment could alleviate these bottlenecks. A shift toward municipal funding using lower-cost capital would enable more affordable housing and faster approvals.

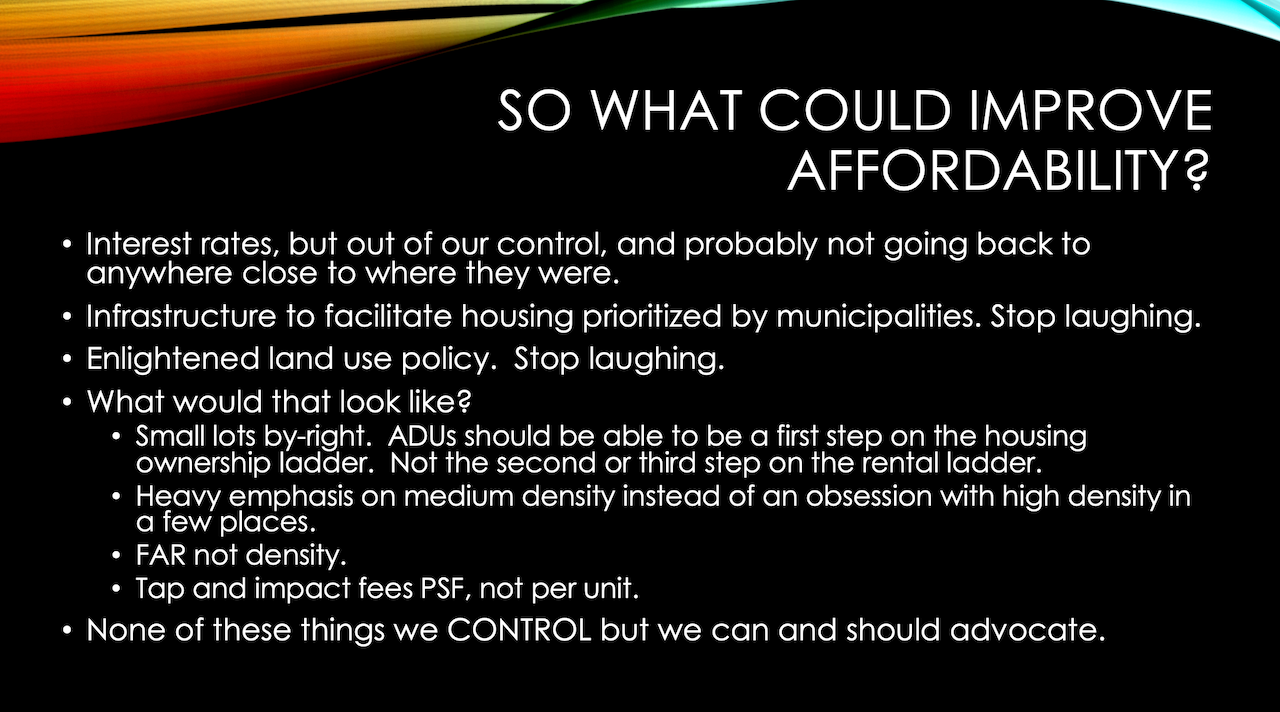

Medium-Density Housing: A Practical Solution

Cox challenges the narrative that suburban development is synonymous with sprawl. Instead, he champions medium-density solutions as a scalable, cost-effective answer to affordability.

- Cost Efficiency:

- Suburban medium-density detached homes: $150 per square foot —affordable and saleable for middle-income buyers.

- Garden apartments: $250 per square foot — less attainable but practical for high-density urban areas.

- Mid-rise apartments: $450 per square foot — luxury pricing, limiting accessibility for most buyers.

- High-rises: $750+ per square foot — prohibitive for broad-scale affordability.

- Key Insight:

We need small-lot detached homes, townhomes, and duplexes to bridge the affordability gap—not an obsession with high-density, high-cost urban development.”

- Suburban areas offer untapped potential for medium-density designs that blend affordability with market demand.

- Recommendation: Builders should prioritize product designs that maximize utility for middle-income buyers, focusing on density that balances cost efficiency and livability.

Entitlement and Land Market Realities

The entitlement process, once a manageable step for private builders, has become prohibitively expensive and time-consuming.

- Challenges:

- Cost Inflation: What once required a $50,000 deposit and processing fee now costs upwards of $500,000 for each step, creating massive barriers for smaller developers.

- Professional Scarcity: A dwindling number of professionals specialize in entitlements, further driving up costs and slowing timelines.

- Capital Reluctance: Institutional investors and banks increasingly avoid funding entitlement processes due to their high risk and upfront costs.

- Impact: Public builders dominate due to their financial resources, leaving private builders struggling to compete in this capital-intensive environment.

- Call to Action: Builders and developers must explore partnerships and collaborative approaches to spread entitlement costs, advocate for streamlined processes, and address talent shortages in the entitlement space.

Lessons for Public and Private Builders

Cox’s presentation highlights how public builders have gained unprecedented advantages through financial discipline, but private builders face mounting disadvantages.

- Public Builders:

- Strengths:

- Low leverage and high cash reserves allow public builders to weather economic downturns and outbid competitors for prime land.

- Long-term covenant-lite debt reduces financial pressure and enables sustained land acquisition and development.

- Aggressive expansion into secondary and tertiary markets broadens their customer base and revenue streams.

- Lesson: Public builders must leverage their capital strength to sustain long-term growth without overextending into speculative projects.

- Their ability to recycle cash and maintain velocity ensures they remain attractive to investors and well-capitalized to adapt to changing markets.

- Strengths:

- Private Builders:

- Challenges:

- Limited access to low-cost capital forces private builders to adopt cautious approaches, often sidelining them in high-velocity markets.

- Rising entitlement and land acquisition costs make it harder for private builders to compete with their publicly financed counterparts.

- Opportunities:

- Niche Markets: Private builders can focus on underserved customer segments, such as first-time buyers or aging Millennials seeking medium-density housing.

- Operational Excellence: By doubling down on efficiency in construction and supply chain management, private builders can deliver more competitive pricing.

- Collaboration: Partnerships with municipalities or joint ventures with public builders can help alleviate financial and operational pressures.

- Challenges:

What It Means and Why It Matters

Scott Cox’s insights highlight a critical inflection point for the industry. Public builders have the resources to weather volatility, but their dominance risks further marginalizing private builders. The sector must address these imbalances to ensure a competitive and dynamic market.

- For Leaders: Advocacy for enlightened land-use policies and infrastructure prioritization is no longer optional—it’s essential.

- For Operations: Medium-density housing and entitlement process innovation are vital levers to unlock affordability and growth.

- For the Industry’s Future: Collaboration between public and private sectors will be key to building resilience and addressing housing’s toughest challenges.

Building Toward Resilience

Despite the immense challenges, Cox concludes on a note of cautious optimism. Affordability, while strained, is not insurmountable. The desire for homeownership remains strong, and the industry is well-positioned to innovate and adapt.

As we approach 2025, the housing industry must double down on its strengths: operational excellence, creative problem-solving, and the relentless pursuit of housing solutions that work for all stakeholders.

With thought- and practice leaders like Scott Cox providing the roadmap, the path forward becomes clearer — and the stakes higher.

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Land

Little Deal ... Big, Timely Product Pivot: Lokal’s Capital Play

A $12M facility fuels Lokal Homes’ swift shift into higher-margin homes and a smarter land strategy in a tough market.

Oversupply or Overreaction? DFW Market Needs To Hit Reset

Scott Finfer breaks down the DFW-area oversupply crisis: post-pandemic assumptions, slower job growth, and mispriced inventory. Across the U.S., high-volume markets face similar risks. Finfer outlines five strategic moves to cut through the noise — and seize ground as bigger players pull back.

Land, Capital, And Control — A New Playbook In Homebuilding

Five Point Holdings’ acquisition of a controlling stake in Hearthstone points to the direction of homebuilding strategy: toward lighter land positions, more agile capital flows, and a far more disciplined focus on vertical construction, consumer targeting, and time-to-market velocity.