Capital

Banking Sector's Shocks Could Work In Housing Market's Favor

"This could be a positive thing for builders and consumers, especially if it causes the Federal Reserve to pause on raising rates, and possibly go so far as to start lowering them before the end of the year. It's a warning shot to the Fed that they went too far too fast on raising rates."

Fallout, shakeout, sell-off blow-out, eke-out, freak-out, not-a-bailout, backstop, extend, pretend, flashback, rinse, repeat.

The terms from experts, analysts, observers, and participants are flying fast and furious, as are the recriminations, allegations, and attacks. The collapse this weekend of not one, but two large regional banks, important for different reasons, has tripped into motion a daisy-chain of reactions, with impacts up and down a stack of interests that tie to housing's already vibrating marketplace.

Here's our bottom line:

- what happened?

- what do our reader executives in homebuilding, real estate, manufacturing, distribution, and related services need to know?

- what does it mean?

- why does it matter?

A day of open markets followed a weekend full of fear and uncertainty. What's clear is that there are more questions than answers ... to all of those initial four questions, especially when it comes to figuring out what these matters will do to an already jittery, fits and starts macro and housing economy.

The crisis in the banking sector also prompted a swift re-evaluation of the number of times the Federal Reserve will raise interest rates, as fears over the resilience of the economy are expected to stay the central bank’s hand.

That led to U.S. government debt markets experiencing their biggest moves since Black Monday in 1987, which was one of the most severe market crashes on record. The two-year Treasury yield, which is sensitive to changes in interest rate expectations, fell 0.54 percentage points in morning trading, to just above 4 percent, its biggest one-day drop since October 1987. – New York Times, Joe Rennison

Here are three snippets from folks we touched base with about how this convulsive event sent a seismic shiver through housing's ecosystem over the past few days.

One, an executive leading the charge on one of homebuilding's vaunted new building technology start-ups, heading just out of early-phase development into a full-fledged test year operating on almost all cylinders:

It was a crazy day yesterday - never thought I'd be involved in a run on a bank - it'll be a story for the ages."

Another friend, a strategic and operational advisor to many homebuilding operators, tells us:

This could be a very positive thing for builders and consumers, especially if it causes the Federal Reserve to pause on raising rates, and possibly go so far as to start lowering them before the end of the year. It's a warning shot to the Fed that they went too far too fast on raising rates."

A third friend, this one a capital investment strategist, note:

The Federal Reserve and Treasury have stepped in and tried to calm the markets as they've shored up the banking system, and we'll just have to see how well their efforts settle down nervous depositors, especially ones whose money exceeds what's normally insured. Together with the cryptocurrency disruption that's played out, there's still risk of more bank instability."

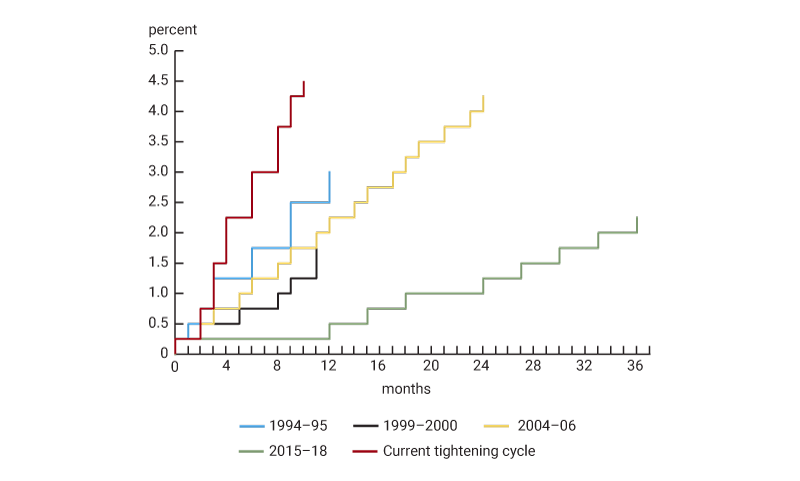

Could there be a better, simpler, more helpful way to put "what happened?" into context than this primitive graphic from Barry Ritholtz' The Big Picture showing Federal Reserve rate increase paths through history:

All you need to focus on from his analysis is that today – at 11 am ET or so – Ritholtz's humble take is that real-time is about learning as opposed to knowing. His list of "what we don't know" stacks up as at least as important to understand as regards impacts on stakeholders like:

- Bank customers – individuals, firms, public and private organizations, investors, etc., both as depositors and borrowers

- Federal officials

- Investors

- Households – wage earners, individual investors, etc.

Confidence, expressed as consumer sentiment, means so much at moments like now. Meanwhile, check out the pretty hefty list of 10 things "we don't know" that The Big Picture's Barry Ritholtz considers essential to sorting things out, at least mechnically and policy-wise, while the issue of confidence evolves from a heightened state of nervousness through its courses toward a collective calm.

10 Unknowns About SVB:

Why did the bank have so much capital wrapped up in long dated Treasuries? Who was advising them? Bond Investing 101 is shorten your duration during a rate hiking cycle – how was this unknown to them?

Why did Peter Theil’s Founder’s Fund (and others) advise companies pull deposits out of SVB? What was the concern? What non-public information did they have beyond the publicly announced capital raise? Were there any other conflicts of interests, legal or otherwise?

How much of this is related to the hangover from the Great Financial Crisis? One aspect of the GFC was junk paper was often not marked to market on a timely basis – the banks “marked to make believe” and created a misleading picture of their solvency. We changed the rules for that. But why are we marking to market Treasury Bonds if they are “money good” at maturity? Should we carve out exceptions to the asset book marks for paper the Fed will repurchase at Par?

What was the impact of the rollback of Dodd Frank in 2018 during the Trump Admin? CEO of SVB had requested – and won – some rule changes, what was their impact? Did that have a material effect on the investment book maintained by SVB? How and in what way?

When did the San Francisco Fed learn SVB/Signature were running into problems? What access did the FRBSF have to the SVB investment book? Did they pass this info on in a timely manner to the Federal Reserve?

Could the regional FRBSF or the Fed itself have helped facilitate a capital raise without disruption? We do not know what was inown when, or

What was the role of messaging here? Did miscommunication from the bank play a role in the subsequent panic?

What was the impact of the most rapid set of rate increases in history have on this event? Was the FOMC a factor in seeing off a bank instability? Was the Fed on both sides of the instability here?

What other banks might have similar issues with their “safe” investment portfolio? What don’t the regulators know about the regionals that they should?

Who ends up owning these banks? Do they become part of a major (Chase, Bof A, Wells Fargo, Citi) or do they stay a regional? What is the purchase price? Shareholders are wiped put, but do bondholder see any capital?

More to learn. Less to know.

ABOUT THE AUTHOR

John McManus, founder and president of The Builder’s Daily, is an award-winning editorial, programming, and digital content strategist. TBD's purpose is a community capable of constant improvement.

MORE IN Capital

Timing Demand: Why Investors Choose To Buy Apartments Vs. Building

A construction slowdown today is setting up an undersupply tomorrow. Opportunistic, patient investors are already pivoting to seize future market growth catalysts.

Little Deal ... Big, Timely Product Pivot: Lokal’s Capital Play

A $12M facility fuels Lokal Homes’ swift shift into higher-margin homes and a smarter land strategy in a tough market.

Land, Capital, And Control — A New Playbook In Homebuilding

Five Point Holdings’ acquisition of a controlling stake in Hearthstone points to the direction of homebuilding strategy: toward lighter land positions, more agile capital flows, and a far more disciplined focus on vertical construction, consumer targeting, and time-to-market velocity.